After reviewing 188 startup applications submitted to the 2026 Global InsurTech Competition, several insurtech trends for 2026 became clear. AI is everywhere — but it is no longer the most interesting differentiator.

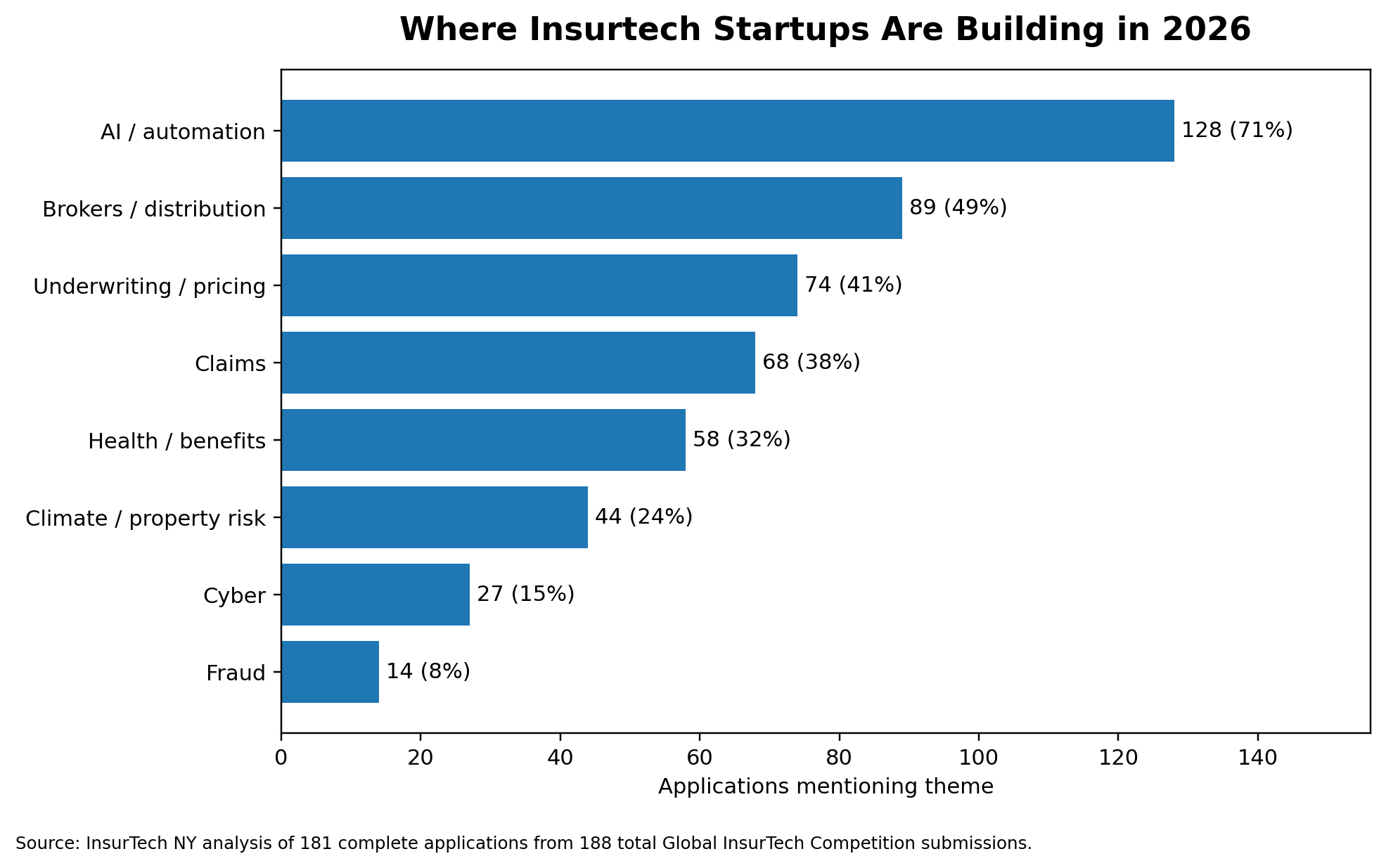

Roughly 71% of applicants referenced AI, automation, machine learning, LLMs, predictive models, agents, or similar technology somewhere in their company description, market category, product explanation, or differentiators.

But that is not the most interesting finding.

The real story is not that startups are using AI. The real story is that AI is becoming infrastructure — a tool embedded inside insurance workflows rather than a standalone pitch.

In the same way that no one wins today simply by being “cloud-based,” startups are no longer differentiated simply because they are “AI-powered.” The stronger companies are using AI to solve highly specific insurance problems: claims leakage, underwriting speed, broker productivity, benefits complexity, fraud detection, property risk, and operational bottlenecks.

Based on 181 complete applications analyzed from 188 total Global InsurTech Competition submissions.

Distribution

Brokers and Agents Are Still Central

Broker, agent, advisor, and distribution-related language appeared across roughly 47% of applications.

That is a useful reminder for the broader technology market: insurance is not only a pricing problem. It is a distribution and trust problem.

Many applicants were not trying to bypass intermediaries. They were building tools to help them quote faster, service clients better, compare options, manage benefits complexity, improve retention, and use AI inside existing workflows.

This is a more mature thesis than the early wave of direct-to-consumer insurtech. Founders appear to understand that brokers and agents still play a powerful role in how insurance is bought, sold, explained, and renewed.

Market Signal

The New Insurtech Playbook Is Less Disruption, More Execution

The early insurtech narrative often centered on replacing legacy carriers, bypassing brokers, or rebuilding insurance from scratch.

This applicant pool felt different.

Many of the strongest startups were not trying to replace the insurance industry. They were trying to make the industry’s hardest workflows faster, smarter, and more defensible.

That is an important shift. The market appears to be moving from broad disruption narratives toward practical execution software: tools for underwriters, claims teams, agents, brokers, benefits administrators, MGAs, carriers, and risk managers.

In other words, the next phase of insurtech may be less about attacking incumbents and more about helping them operate better.

Claims

Claims Is One of the Clearest Battlegrounds

Claims appeared across roughly 38% of the applications, making it one of the most active themes in the dataset.

That makes sense. Claims is where insurers face some of their most visible and expensive pain points:

Manual workflows

Slow response times

Fraud risk

Litigation exposure

Customer dissatisfaction

Loss adjustment expense

Operational inconsistency

Startups are attacking the category from multiple angles, including claims intake, fraud detection, adjuster support, litigation analytics, repair coordination, document review, workflow automation, and customer communication.

The takeaway: claims is no longer just a back-office function. It is becoming a strategic technology battleground.

Underwriting

Underwriting Is Being Augmented, Not Replaced

Underwriting, pricing, risk selection, quoting, and submission workflows appeared in roughly 42% of applications.

But the strongest signal was not “AI will replace underwriters.” It was more practical than that.

Founders are building tools to help underwriting teams move faster, evaluate risk more consistently, enrich submissions, identify better signals, and reduce manual review.

That distinction matters. Insurance still rewards judgment, domain knowledge, and accountability. The startups that understand this are not trying to remove the human from the process. They are trying to give the human better tools.

The best underwriting startups are not selling replacement. They are selling leverage.

Business Model

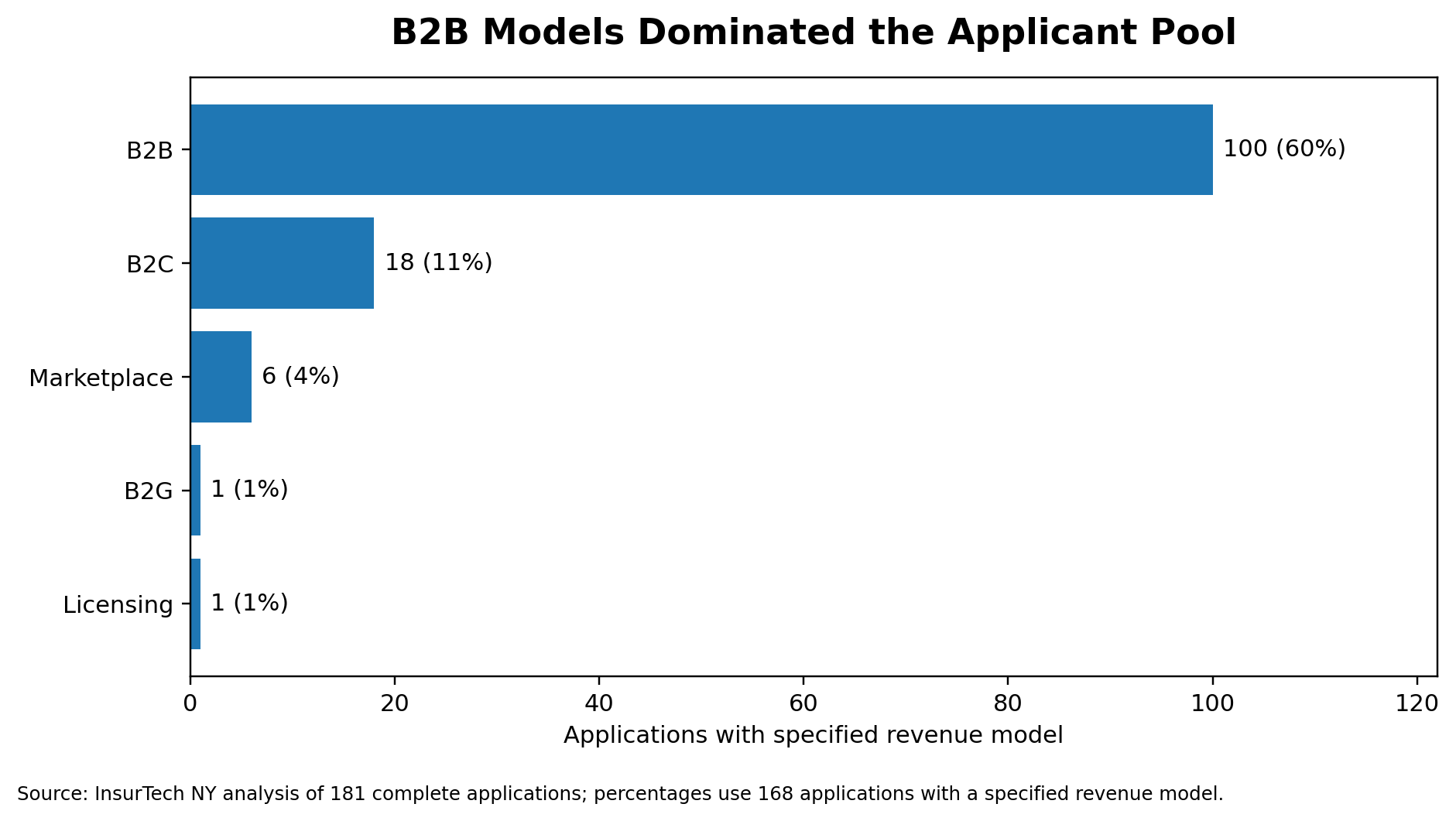

B2B Is Dominating the New Wave

Among applicants with a specified revenue model, B2B was the most common category by a wide margin, with 100 companies listing B2B as their model.

This may be one of the most important signals in the data.

The current startup wave appears less focused on expensive consumer acquisition and more focused on selling software, infrastructure, and intelligence to organizations that already have customers, licenses, distribution, capital, and trust.

That does not mean consumer insurance innovation is gone. But it does suggest that many founders see the clearest opportunity inside the insurance value chain, not outside of it.

B2B models dominated the applicant pool, reinforcing the shift toward tools built for insurers, brokers, MGAs, and enterprise buyers.

Traction

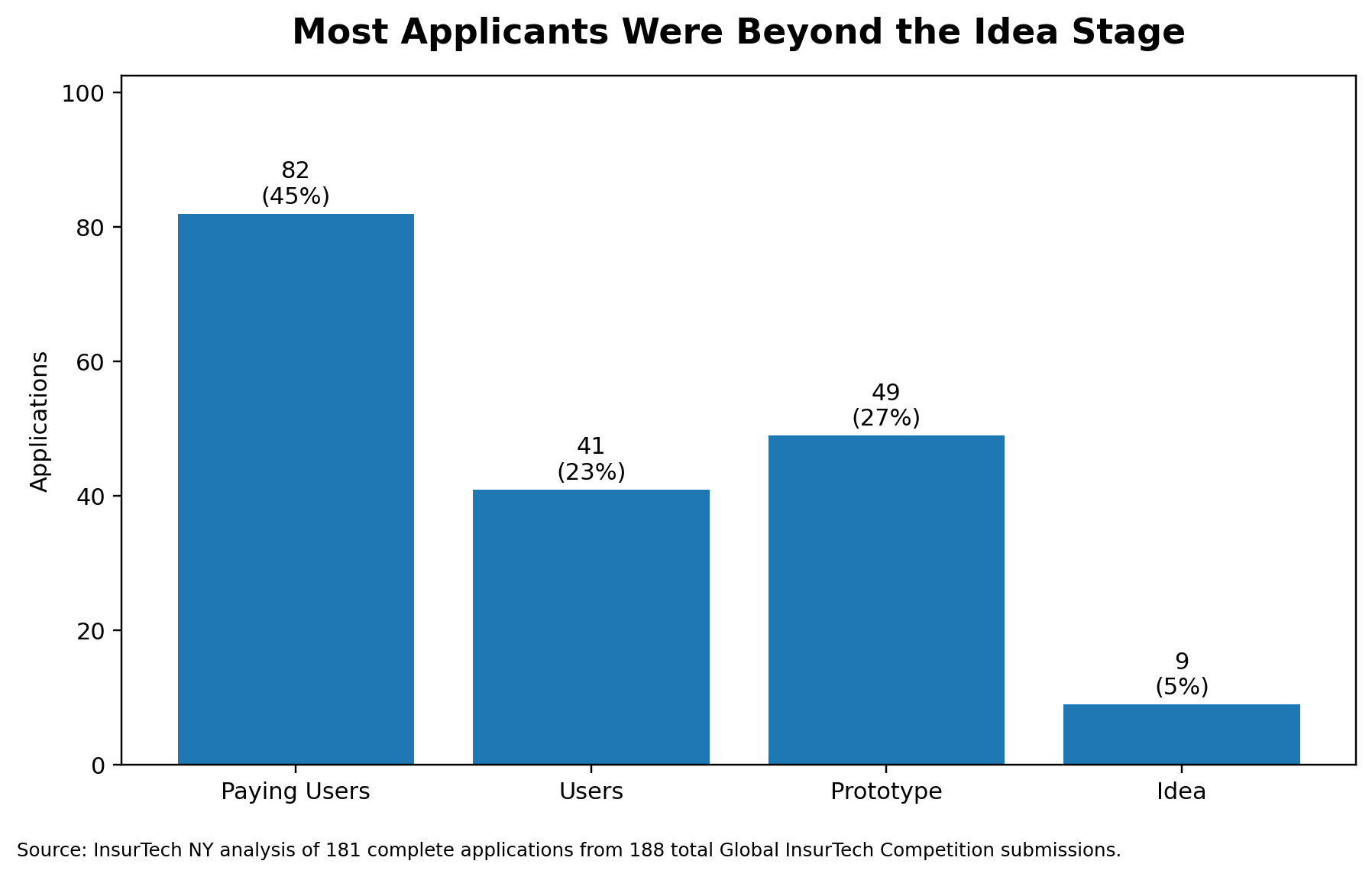

Most Applicants Were Building Real Businesses, Not Just Concepts

This was not a field dominated by napkin-stage ideas.

Of the 181 applicants, 82 reported paying users, 41 reported users, 49 were at prototype stage, and only 9 were at the idea stage.

That matters because it suggests the market is becoming more disciplined. Founders are being pushed to show traction, not just vision.

For investors, carriers, and partners, the key questions are becoming sharper:

Who is already using this?

What workflow has changed?

What cost has been reduced?

What risk has been improved?

What evidence exists beyond the pitch?

That is a healthier market than one built purely on hype.

Most applicants were beyond the idea stage, with a large share already reporting users or paying users.

Global View

Insurtech Innovation Is Increasingly Global

The United States led the applicant pool with 90 companies, but the competition drew applications from 37 countries.

That global spread is important. Insurance pain points may be universal, but market conditions vary widely. In some regions, founders are building around legacy infrastructure. In others, they are solving for underinsurance, distribution gaps, climate exposure, health access, regulatory complexity, or fragmented data.

The next breakout insurtech companies may not all come from the same familiar hubs. Some may emerge from markets where inefficiencies are sharper and the need for new infrastructure is even more urgent.

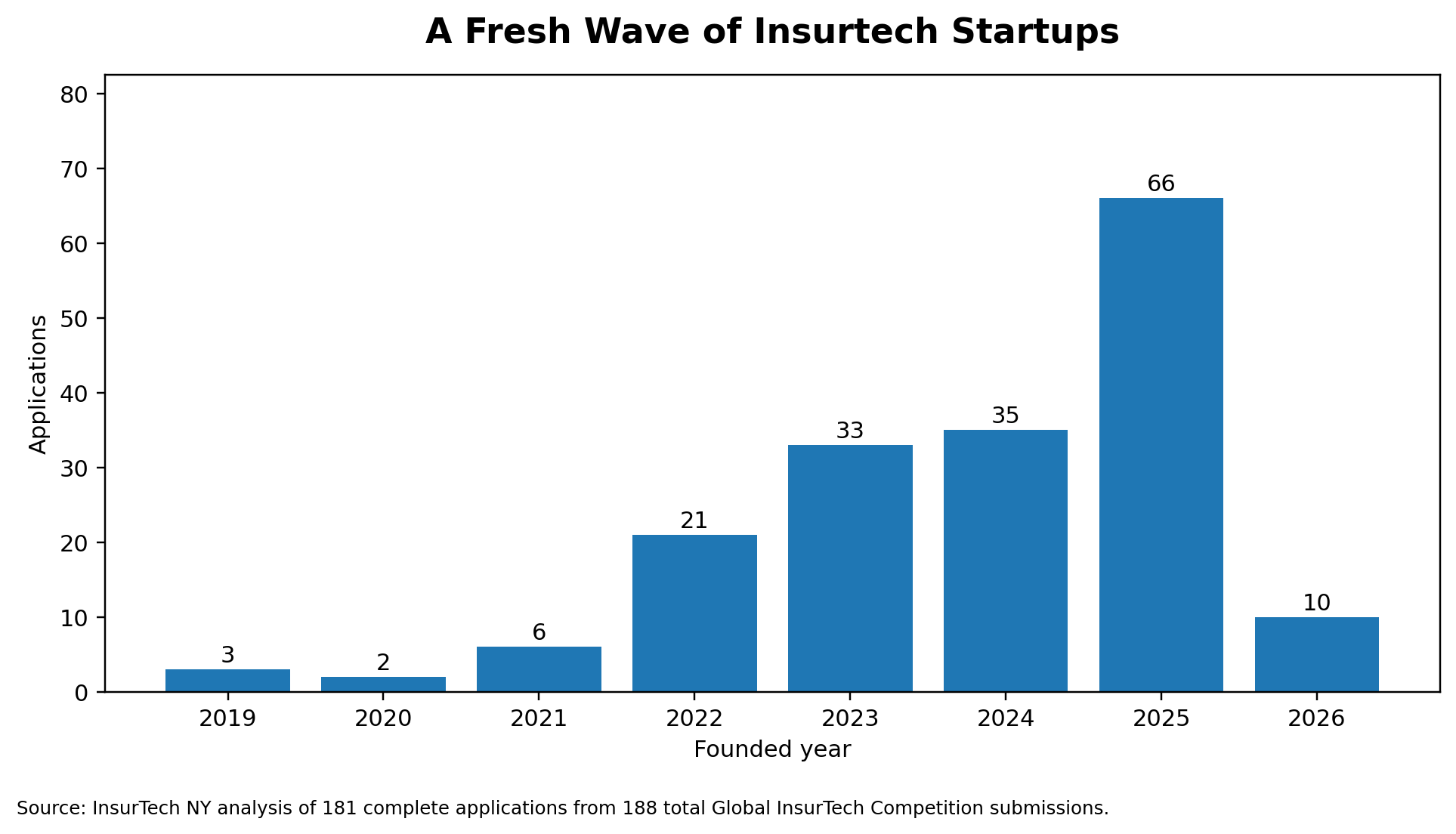

The founding-year data points to a fresh wave of insurtech startups, many shaped by the recent acceleration of AI and workflow automation.

Emerging Themes

Beyond AI: The Themes Worth Watching

When we looked past the AI language, several deeper market themes stood out.

Health and benefits appeared across roughly 37% of applications, reflecting continued complexity in healthcare, employee benefits, ICHRA, medical access, and insurance administration.

Climate, property, weather, flood, wildfire, and catastrophe-related themes appeared across roughly 22% of applications, reinforcing the growing connection between insurance innovation and physical risk.

Cyber appeared across roughly 14% of applications, while fraud appeared across roughly 8%. These categories may be smaller by volume, but they remain strategically important because they sit directly at the intersection of risk, data, and underwriting discipline.

The broader takeaway is clear: “AI for insurance” is too generic. The best opportunities are forming where AI meets a specific insurance pain point.

Final Takeaway

Insurtech Is Growing Up

The applications suggest a market entering a more mature phase.

The next generation of insurtech startups is not simply trying to sound futuristic. Many are building practical tools for the operational realities of insurance: underwriting, claims, distribution, benefits, risk selection, compliance, and workflow execution.

AI is everywhere now. That is no longer the interesting part.

The interesting part is whether founders understand insurance deeply enough to apply AI where it actually matters.

The startups most likely to define the next phase of insurtech will not be the ones with the loudest AI story. They will be the ones that solve painful insurance problems with precision, credibility, and measurable impact.

These insurtech trends for 2026 suggest a more mature market focused on execution, underwriting efficiency, claims transformation, and practical AI adoption.

Newsletter Signup

Sign up today and be at the forefront of the insurance transformation. Together, we’re not just keeping up with the future; we’re making it.

Upcoming Events & Programs

InsurTech NY events bring together carriers, brokers, startups, and investors to facilitate new relationships and share insights from insurance influencers.